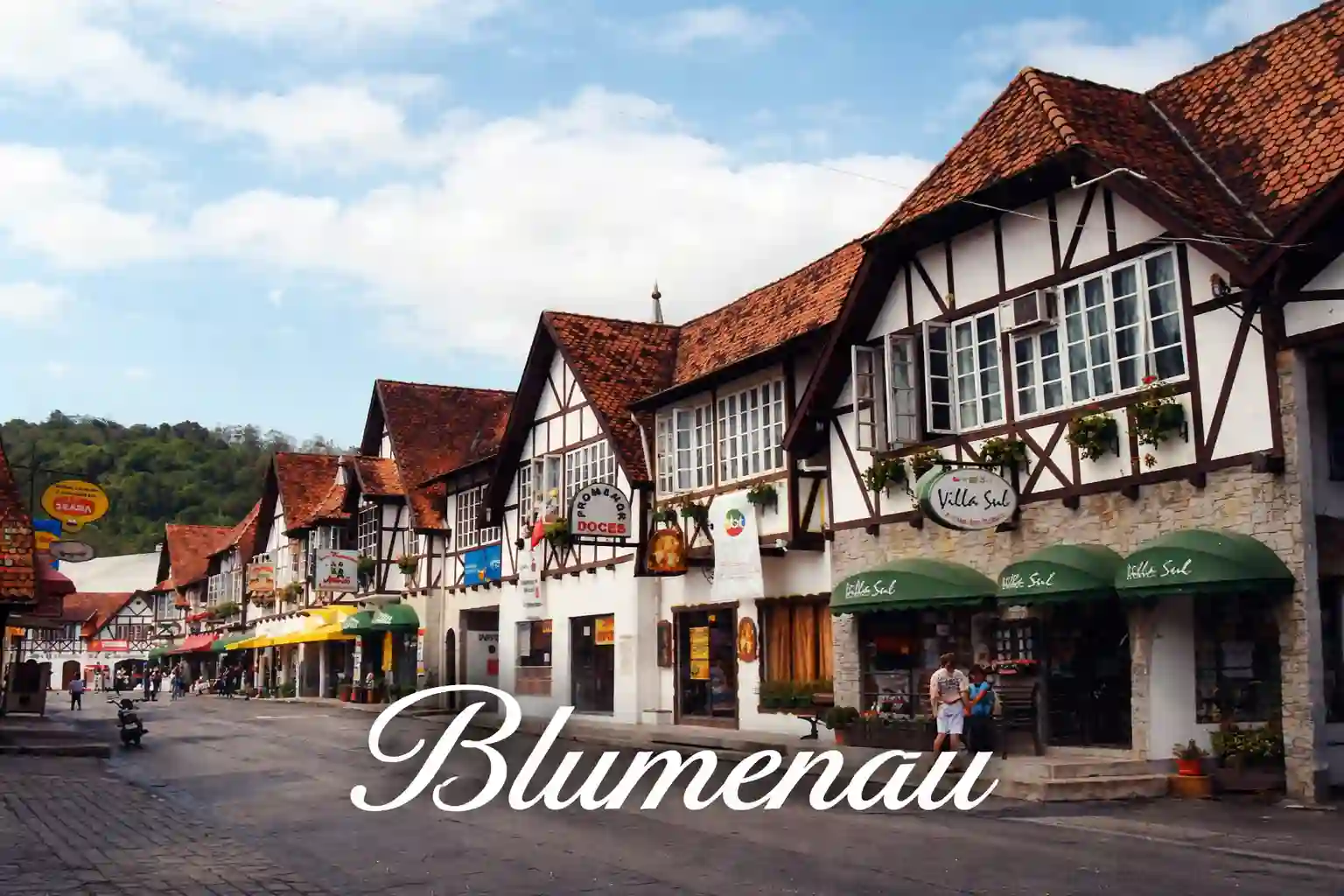

Blumenau and the

Long View: What the

Itajaí Valley Reveals

About Industrial Continuity

Santa Catarina posted Brazil's highest industrial growth rate in 2024 — 7.7%, more than double the national average. Blumenau and the Itajaí Valley are where that structural pattern is most legible: a settlement history that produced a specific kind of enterprise culture, and a question about how much of that history still explains what the data shows today.

In 2024, Santa Catarina's industrial production grew by 7.7 percent — the highest rate of any Brazilian state, according to IBGE data, and more than double the national average of 3.1 percent. The sectors that drove it included machinery and equipment, electrical components, and capital goods production. These are not new industries in the region. They are the latest iteration of an industrial structure that has been building for nearly 175 years in the valleys of southern Brazil's most consistently outperforming state.

Understanding why requires going back to 1850, and to a specific kind of economic actor: not the colonial plantation, not the extractive venture, but the craftsman-entrepreneur.

Immigration as Industrial Foundation — and Its Limits as an Explanation

When Hermann Bruno Otto Blumenau organised the colonisation of the Itajaí Valley in 1850, he brought no capital strategy. He brought craftsmen, small farmers, and traders from the German-speaking world — people who arrived with technical skills, a work culture structured around artisanal mastery, and a model of enterprise oriented toward family continuity rather than short-term returns. The settlement of what is now the greater Blumenau region, along with Joinville, Jaraguá do Sul, and Brusque, coincided with the second phase of European industrialisation, which meant that many of the new arrivals were already familiar with small-scale manufacturing, metalworking, and textiles.

What emerged over the following generations was not a replica of European industrial organisation transplanted to the tropics, but a pragmatic adaptation under specific conditions — periodic flooding, geographic isolation from Brazil's main markets, and the absence of the large-scale plantation economy that shaped other Brazilian regions. The companies that endured were, almost without exception, family-controlled, regionally anchored, and oriented toward long time horizons. Whether that pattern is a product of ethnic continuity, geographic necessity, or simple selection — the enterprises that could not adapt did not survive — is genuinely difficult to disentangle, and the honest answer is probably all three.

"The Hering company was founded in 1880 by German immigrant brothers. Döhler, now 143 years old with around 3,000 employees, traces its origin to the same wave of settlement. Wetzel, in precision casting, has remained under the original family's direction since 1932. These are not historical footnotes. They are operating companies."

What the Industrial Structure Actually Looks Like

The greater Santa Catarina industrial cluster — centred on the Itajaí Valley but extending through Joinville in the north and Jaraguá do Sul in the hinterland — is built around sectors that require accumulated technical knowledge rather than scale alone: precision machinery, electrical components and transformers, textiles and technical fabrics, food processing ingredients, and metalworking. Blumenau's top exports in 2023 were electrical transformers (USD 59.5 million), electrical control boards (USD 47.2 million), and vehicle parts (USD 14.7 million), according to data from the Observatory of Economic Complexity.

The state is also, critically, a deep industrial importer — Santa Catarina was Brazil's second-largest importer in 2024 at USD 33.7 billion, behind only São Paulo. That figure is not a weakness; it reflects the density of industrial inputs flowing into manufacturing operations that process and re-export finished and intermediate goods. It is the signature of an economy oriented toward industrial transformation, not just assembly.

The comparison often drawn to the German Mittelstand is worth treating carefully. It is functionally accurate in one specific sense: the long-established companies of the Itajaí Valley share the defining structural characteristic of owner-managed, long-horizon businesses — planning cycles measured in decades, competitive advantage embedded in accumulated technical knowledge. But the comparison risks overstating cultural transmission and understating the role of economic geography, regulatory history, and simple survival selection. What can be said with confidence is that the outcome resembles the Mittelstand pattern — and that this resemblance is observable in how companies here behave during macroeconomic stress.

The Santa Catarina Divergence

Between 2002 and 2023, Santa Catarina's share of Brazilian national GDP grew by one full percentage point — from around 3.7 percent to 4.7 percent. That is a sustained structural shift, not a cyclical spike. Over the same period, São Paulo's share of national GDP fell by 3.4 percentage points and Rio de Janeiro's fell by 1.7 percentage points, according to IBGE regional accounts data. The South gained; the traditional industrial and financial centres of the Southeast lost ground in relative terms.

That divergence is partially explained by commodity cycles — Mato Grosso and other agricultural states also gained share over the period. But Santa Catarina's shift is specifically industrial. The 2024 IBGE data showing 7.7 percent industrial growth is consistent with a longer pattern: in 2021, during the pandemic recovery, Santa Catarina also led Brazil with 10.3 percent industrial growth. The consistency of the outperformance points to structural factors, not just favourable conditions in a given year.

What Blumenau Itself Exports

Blumenau is the most internationally recognised name in the region, but it is worth being precise about what it actually produces. The city's export profile — electrical transformers, control systems, vehicle components, and machinery — reflects the capital goods focus of the broader Itajaí Valley cluster. These are products sold to other industries, not to end consumers. They are precisely the kind of intermediate industrial goods that underpin production capacity across South America. The region's top export destinations in early 2024 included the United States, Canada, and Bolivia — a mix of developed-market industrial buyers and regional supply chains.

At the same time, Blumenau imports heavily from China — synthetic textile inputs, steel, and electronic components that feed its manufacturing processes. The city runs a trade deficit in merchandise terms. Its value is not in raw export volumes, but in the industrial capability that transforms those inputs into finished capital equipment.

The Limits of the Model

The German-Brazilian industrial model of Santa Catarina is not without friction. Severe flooding — the region sits in a river valley prone to inundation — has periodically disrupted production, most recently in 2023 and in the catastrophic 2008 event. Infrastructure investment has not always kept pace with industrial growth. The cultural closeness that makes long-term business relationships durable also creates barriers to external entry that can limit the speed of capital formation and technology adoption.

Hering, perhaps the most globally recognisable brand in the cluster, was founded in 1880, acquired by Arezzo in 2022, and is now part of a larger Brazilian fashion conglomerate — a transition that illustrates both the generational limits of family ownership models and the appetite of Brazilian capital for the region's established brands. That acquisition is itself a data point: the value built over 140 years of family management was legible enough to attract a significant acquisition premium in the Brazilian market.

What Santa Catarina demonstrates, viewed as a whole, is a consistent pattern: a state with a specific settlement history, a dense concentration of family-owned industrial enterprises, and a track record of outperforming the Brazilian national average on industrial metrics over multiple cycles. Whether the settlement history directly causes the economic performance, or whether both reflect deeper geographic and structural factors, is a question that data alone cannot fully resolve. What the data does show — in the 7.7 percent industrial growth of 2024, in the sustained GDP share gains since 2002, in the survival of companies founded in the 1880s — is that something in the structure of this economy produces durable industrial output. That is a different kind of economic foundation than most of Latin America has built. And it is worth understanding on its own terms, without over-explaining it.