Chile · Venezuela · Earthquake Risk · Infrastructure Resilience · Investment

Two Earthquake Economies, Two Risk Profiles: What Chile and Venezuela Reveal About Infrastructure Investment

Earthquakes are geological events. For investors, they become infrastructure tests. Chile shows how seismic risk can be institutionalized through codes, protocols and financial protection. Venezuela shows how the same category of shock can expose weaker buildings, grid stress, public-infrastructure limits and reconstruction capacity.

Chile and Venezuela show two different earthquake economies.

Chile is a high-seismic-risk country where earthquakes are translated into engineering practice, emergency protocols, mining inspections and financial protection. Venezuela’s June 2026 earthquakes show a different risk profile: oil production and export infrastructure appeared comparatively resilient, while damaged buildings, power outages, public infrastructure, port constraints, airport disruption and reconstruction capacity exposed weaker parts of the system.

The investment signal is clear. Earthquake risk is not judged only by magnitude. It is judged by the ability of infrastructure, institutions and public finance to absorb stress.

For related context, see Econosur’s Chile market insights, energy and infrastructure coverage, mining sector analysis and South America Sector Briefs.

Core market reading:

Natural hazards become investment signals when they touch buildings, ports, mines, power grids, airports, hospitals, public budgets and insurance capacity.

Chile shows how repeated seismic exposure can become a governance and engineering discipline. Venezuela shows how a major earthquake can reveal a split risk profile: strategic oil infrastructure may hold, while the built environment, grid and public systems expose deeper resilience deficits.

Why Compare Chile and Venezuela?

Venezuela is not a Cono Sur economy. That is exactly why the comparison has to be framed carefully. Venezuela is the current shock case. Chile is the South American benchmark for living with major earthquake risk.

The comparison is not geographic branding. It is an infrastructure-investment question. How do countries convert seismic exposure into building codes, emergency routines, fiscal buffers, insurance mechanisms and operational protocols? How does the same class of natural hazard behave when it meets weaker buildings, stressed public infrastructure and limited system redundancy?

Chile and Venezuela sit on different tectonic systems. Chile’s strongest earthquake risk is associated with the subduction of the Nazca Plate beneath the South American Plate along the Pacific margin. Venezuela’s northern seismic risk is linked to the boundary between the Caribbean Plate and the South American Plate. The investor question is not whether the tectonics are identical. The investor question is how institutions absorb seismic stress.

"Earthquakes do not create the whole investment risk. They reveal how much risk was already inside the infrastructure system."

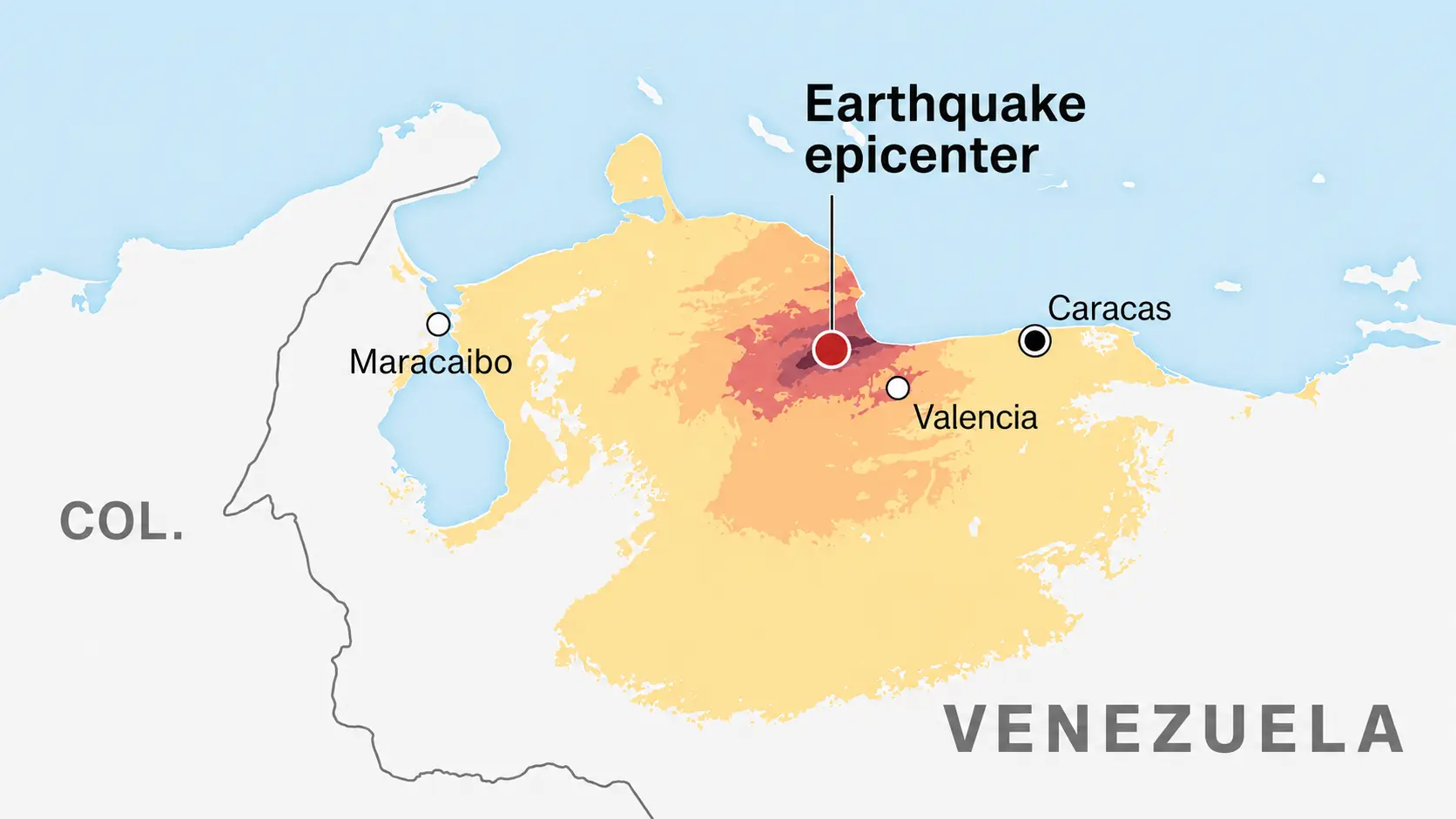

Venezuela: When a Seismic Shock Exposes the Built Environment and the Grid

The June 2026 Venezuela earthquakes created a brutal human emergency. For infrastructure investors and B2B suppliers, they also produced a more precise market signal: the oil-export system appeared more resilient than the built environment, the power grid, public infrastructure and emergency logistics.

Reuters reported that Venezuela’s crude production remained around 1.2 million barrels per day after the quakes and that key oilfields and export terminals were largely untouched. An initial Reuters report also said that Venezuela’s oil infrastructure did not immediately appear to be affected by the tremors, with a worker at the El Palito refinery near Morón reporting no damage there.

That makes the Venezuela signal sharper, not weaker. The earthquake did not simply show a collapsed oil sector. It showed a split risk profile: oil production and export infrastructure held comparatively well, while power outages, damaged buildings, port constraints, airport disruption and emergency-response capacity exposed the fragility of the wider infrastructure system.

UNDP estimated preliminary direct physical damage at US$6.7 billion, with a range of US$4.7 billion to US$8.7 billion. UNDP also stressed that this figure excludes infrastructure damage, wider economic disruption and longer-term reconstruction costs. The initial damage estimate is therefore only the first layer of the infrastructure bill.

The market point is precise. Venezuela’s earthquake risk became an infrastructure-risk signal because the event exposed the condition of housing, public infrastructure, electricity transmission, logistics and reconstruction capacity. The oil system matters in the article because it provides the contrast: not every asset class failed in the same way.

Damaged and collapsed buildings in Caracas and La Guaira made the earthquake primarily a housing, construction-quality and public-safety crisis rather than a pure oil-sector crisis.

Power outages and damaged transport infrastructure complicated recovery, port operations, hospitals, aid distribution and the restoration of normal public services.

Oil production and key export infrastructure appeared comparatively resilient. That contrast makes the wider infrastructure gap more visible: the weakest signal was not crude output, but the built environment and the grid.

Chile: A Seismic Economy With Institutional Memory

Chile’s earthquake profile is severe, but its investment profile is different. Chile has turned repeated seismic exposure into engineering practice, public procedures, risk modeling and financial instruments.

The National Institute of Standards and Technology published a detailed comparison of U.S. and Chilean building code requirements and seismic design practice from 1985 to 2010. The report was part of investigations into the performance of engineered construction during the February 27, 2010 Maule earthquake and was intended to draw conclusions from observed building performance in Chile.

That matters because it shows an institutional learning loop. Earthquakes are not treated as isolated events. They become evidence for design practice, construction requirements, structural review, emergency rules and future adjustment.

A recent operational example came from northern Chile. Reuters reported that a May 2026 earthquake in the Antofagasta mining region disrupted some operations but caused minimal damage. Codelco halted some activities due to lack of visibility in pits or electricity interruptions in specific areas, while BHP and Antofagasta said their operations were not affected.

That is the difference investors watch. The same natural hazard category can cause temporary inspections and localized interruptions in one country, while exposing cascading infrastructure fragility in another.

Why Companies Like Codelco, BHP and Antofagasta Matter in This Story

Company names should be used carefully in earthquake-risk analysis. The point is not to claim that one company is safe or another company is exposed. The point is to show how operational resilience becomes visible when a strong earthquake hits a production region.

Chile’s mining sector is a useful example because copper, lithium, water supply, power systems, roads, rail, ports and worker safety are all connected. Codelco, BHP and Antofagasta Minerals operate in a country where seismic exposure is normal business reality. When Reuters reports that emergency protocols were activated, some activities were halted for inspection and major operators reported limited or no operational impact, that becomes a signal about system maturity.

For investors, the relevant question is not whether an earthquake occurred. The relevant question is whether companies, regulators, contractors and infrastructure operators know what to do when it occurs.

That same logic applies to Venezuela, but the visible actors are different. The relevant layer is not a mining company. It is the national power grid, the building stock, ports such as Puerto Cabello and La Guaira, airport operations, public infrastructure and the emergency logistics system. El Palito and other oil assets are relevant mainly as a contrast: early reporting suggested limited direct damage to core oil infrastructure, while electricity and public infrastructure became the more visible stress points.

| Market layer | Chile signal | Venezuela signal |

|---|---|---|

| Industrial operations | Mining operators can inspect, pause and resume within a known seismic-risk environment. | Oil production and key export infrastructure appeared comparatively resilient, while other systems showed greater stress. |

| Built environment | Seismic design practice and code iteration reduce the probability that strong earthquakes become uncontrolled building-collapse events. | Damaged and collapsed buildings in Caracas and La Guaira exposed the vulnerability of housing stock and public infrastructure. |

| Critical infrastructure | Power, roads, mine sites and emergency protocols are part of the resilience system. | Electricity, ports, airport functions, hospitals, emergency logistics and communications became immediate bottlenecks. |

| Investment meaning | Seismic risk is priced into engineering, operations and fiscal protection. | The earthquake revealed a split profile: some strategic oil assets held, while the grid and built environment exposed broader resilience deficits. |

The Infrastructure-Resilience Test for Investors

For infrastructure investors, earthquake exposure is only the starting point. The deeper test is how a country’s infrastructure behaves under stress.

Buildings are the first test because weak construction immediately turns seismic energy into human loss, emergency shelter demand and reconstruction cost. Power grids are the second test because energy disruption quickly affects hospitals, fuel systems, ports, airports, water supply and industrial production. Ports and transport corridors are the third test because imports, emergency equipment, food, fuel and reconstruction materials depend on them.

Public finance is the fourth test. Reconstruction requires money before the full economic loss is visible. A country with fiscal buffers, insurance instruments, market access and institutional capacity can respond differently from a country already under fiscal or debt pressure.

Chile’s Catastrophe Bond Shows the Financial Layer

Chile’s resilience profile is not only physical. It also has a financial layer.

In 2023, the World Bank executed a US$630 million catastrophe bond and swap transaction that provided earthquake insurance coverage to the Government of Chile. The structure combined US$350 million of catastrophe bonds and US$280 million of catastrophe swaps. The stated purpose was to mitigate disruptive economic impacts, make funds available after a disaster, protect Chile’s fiscal budget and reduce the potential need to mobilize debt after an event.

The transaction also shows who reads this market signal. Aon Securities, GC Securities, Swiss Re Capital Markets and AIR Worldwide were named in the World Bank release as part of the transaction’s structuring, risk modeling and distribution ecosystem.

That matters for B2B markets. Earthquake resilience creates a demand field around insurance-linked securities, catastrophe modeling, risk engineering, public-sector finance, infrastructure assessment, emergency logistics, construction standards and monitoring.

Investment interpretation:

Chile’s advantage is not the absence of earthquake risk. Chile’s advantage is the conversion of earthquake risk into standards, protocols and financial instruments that investors can understand.

What B2B Suppliers Should Read From This

Earthquake resilience is a B2B market. It includes engineering services, structural assessment, grid stabilization, monitoring systems, emergency power, sensors, industrial automation, port logistics, risk modeling, insurance, consulting, technical documentation and specialist translation.

Suppliers that serve mining, energy, ports, utilities, construction, insurance or public infrastructure should read earthquake events as market intelligence. The question is where resilience gaps become visible, which assets are stressed first and which technical categories move from optional upgrade to procurement priority.

For German-speaking technical suppliers, documentation can also become part of the market. Geological studies, structural assessments, risk reports, environmental reports, manuals, inspection protocols and emergency documentation need precise language when projects operate across Spanish, English, German and Portuguese contexts. That is why specialist geoscience translation by eLengua is linked here as a related professional layer, separate from Econosur’s market analysis.

- Which South American infrastructure assets are most exposed to earthquake-related building, power, logistics or operational disruption?

- Which mining regions have strong emergency protocols and which depend on weaker public infrastructure?

- Which ports, airports, refineries, power plants and industrial corridors become stress points after major seismic events?

- Which insurers, reinsurers, brokers and catastrophe-risk modelers are already visible in South American resilience finance?

- Which technical suppliers appear in search and AI-generated answers for earthquake resilience, grid stability, structural assessment and emergency systems?

- Which geological, engineering and risk documents require specialist translation for cross-border infrastructure projects?

The Econosur Reading

The Chile-Venezuela comparison is a warning against treating natural hazards as background geography.

For South American infrastructure investors, earthquakes are market tests. They test the built environment, the power grid, construction quality, industrial redundancy, ports, airports, hospitals, public communication, damage assessment, insurance capacity and fiscal response.

Chile shows how a country can build an investment profile around repeated exposure. Seismic risk becomes part of building practice, mining operations, emergency management and public-finance strategy. Venezuela shows how a major earthquake can expose a split infrastructure profile: the oil-export system may hold better than expected, while buildings, public infrastructure, logistics and the power grid reveal deeper vulnerability.

This is the broader South American lesson. Investors should not ask only where earthquakes happen. They should ask where infrastructure can keep functioning, where data is credible, where response finance exists and where industrial suppliers can reduce the next bottleneck.

"The strongest earthquake economy is not the country without earthquakes. It is the country that turns seismic reality into infrastructure discipline."

This article uses market reporting, official sources, technical research and financial-risk documentation available in June 2026. The analysis distinguishes confirmed reporting from broader investment interpretation.

- Reuters — Two major earthquakes strike Venezuela.

- Reuters — Venezuela oil output steady after quakes; power outages persist.

- UNDP — Venezuela faces US$6.7 billion in economic losses from earthquakes.

- Reuters — Strong Chile earthquake shakes mining hub, but damage is minimal.

- NIST — Comparison of U.S. and Chilean building code requirements and seismic design practice 1985–2010.

- WCEE 2012 — Chilean Emergency Seismic Design Code for Buildings after El Maule 2010 Earthquake.

- World Bank — Chile US$630 million catastrophe bond and swap transaction.

- eLengua — Geoscience translation for technical and geological documentation.

From natural hazard to infrastructure-risk intelligence

South America’s infrastructure markets are shaped by more than growth forecasts. Earthquakes, floods, droughts, energy stress and logistics bottlenecks reveal which systems can absorb shocks and which systems transmit them into investment risk.

Econosur prepares custom market analysis for companies, investors and institutions evaluating infrastructure resilience, mining regions, energy systems, ports, industrial suppliers and market-entry strategy across South America.

Explore custom market analysisFAQ

Why compare Chile and Venezuela in an infrastructure-investment analysis?

Chile and Venezuela are both exposed to seismic risk, but they show different risk profiles. Chile demonstrates how earthquake risk can be translated into codes, emergency protocols and financial protection. Venezuela shows how a seismic shock can expose weaker parts of the built environment, power-grid fragility and public-infrastructure pressure, even when oil production and export infrastructure appear comparatively resilient.

What makes Chile a useful earthquake-resilience benchmark?

Chile is one of the world’s most seismically active countries and has developed earthquake-resistant building practice, emergency protocols and financial risk-transfer tools. Its response to recent mining-region earthquakes shows how operational disruption can be limited when infrastructure systems and institutional procedures are mature.

What did the June 2026 Venezuela earthquakes reveal for investors?

The Venezuela earthquakes revealed that natural hazards become investment signals when they expose differences between asset classes. Oil production and key export infrastructure appeared comparatively resilient, while damaged buildings, power outages, port constraints, airport disruption and public-infrastructure stress exposed the weaker parts of the system.

Which companies are relevant to this risk profile?

Mining companies such as Codelco, BHP and Antofagasta Minerals are relevant on the Chilean side because mining operations depend on resilient power, water, roads and emergency protocols. Energy, port, refinery and petrochemical infrastructure is relevant on the Venezuelan side, especially as a contrast between comparatively resilient oil assets and weaker public infrastructure. Reinsurers, brokers, catastrophe-risk modelers and infrastructure investors are relevant because they price and finance resilience.

Why does earthquake risk matter for B2B suppliers?

Earthquake risk creates demand for engineering, grid resilience, monitoring, emergency systems, structural assessment, insurance, risk modeling, industrial automation, technical documentation and localized compliance communication. Suppliers that understand this risk language can position themselves more clearly in South American infrastructure markets.